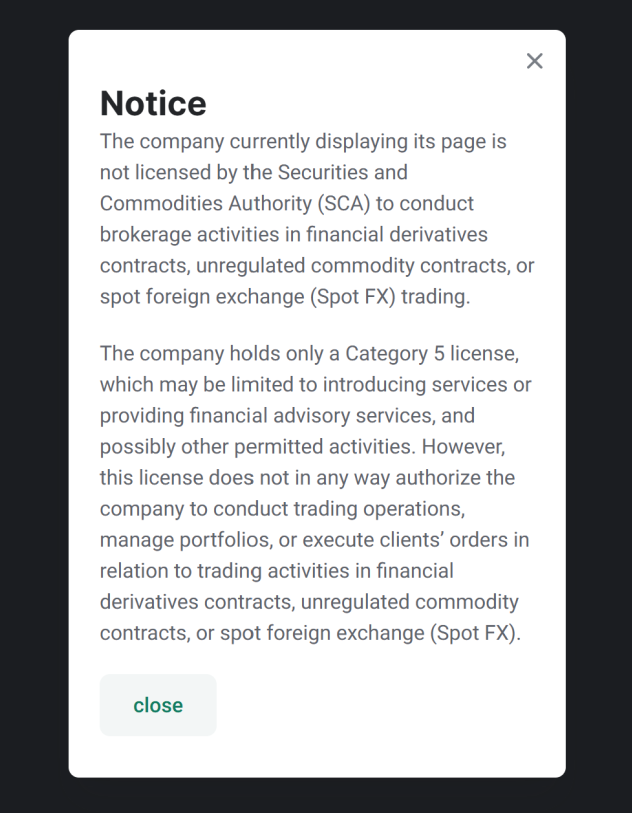

The UAE financial services market has witnessed a sharp increase in the number of firms operating under Category 5 licenses issued by the Securities and Commodities Authority (SCA). What initially appeared to be a “lighter” category of financial services licensing has now become one of the most debated and misunderstood segments within the UAE financial ecosystem. Category 5 licensed entities are generally involved in activities such as Introduction, Promotion, and Financial Consultation/Analysis. A firm may hold one activity or a combination of multiple activities under the same license structure.

On paper, the scope may appear straightforward. However, in practice, Category 5 businesses operate in one of the most sensitive regulatory grey zones within the UAE market.

The confusion does not arise because the laws are absent. The confusion exists because the business models are evolving faster than the market’s understanding of regulatory expectations.

Understanding Category 5 Activities

At a practical level, most Category 5 firms act as intermediaries between clients and regulated financial institutions. These entities “are not allowed” to execute trades, hold client funds, or maintain custody of client assets. Yet, they remain deeply connected to client onboarding, investor communication, and investment decision influence.

This is where the complexity begins.

Many market participants incorrectly assume that because Category 5 entities do not physically hold client money, they are outside the strict perimeter of financial crime compliance obligations. That assumption is dangerous.

Under UAE law, these entities are still categorized as Licensed Financial Institutions (LFIs), and therefore many AML/CFT obligations continue to apply irrespective of whether the client funds touch their accounts or not.

Introduction vs Promotion — The Thin Line

One of the biggest issue in the market is that the practitioner can’t even differentiate between “Introduction” and “Promotion”. On paper, the difference appears simple.

An Introducing Activity involves merely connects a client to another regulated financial institution. The client relationship, execution, onboarding, and operational handling are expected to remain with the receiving regulated entity.

Promotion, however, goes a step further. Promotion involves marketing, influencing, encouraging, or persuading potential investors regarding financial products or services.

The challenge is that in real market practice, these two activities often overlap and firms are unable to file the P&L Activity reports properly as per Article 7(1), Chapter 5, Section 2 of the SCA Board Chairman’s Decision No. (13/Chairman)

A simple WhatsApp message, social media post, webinar discussion, trading seminar, or sales call can unintentionally cross the line from “introduction” into “promotion.”

The moment a representative starts discussing product performance, potential returns, market opportunities, or comparative advantages, regulatory exposure increases significantly. This is why many firms also struggle during inspections. A company may internally believe it is “only introducing clients,” while its actual communication style, marketing materials, sales behavior, and client interaction patterns may reflect promotional conduct.

The issue becomes even more sensitive in digital marketing environments where sales teams operate aggressively through Telegram groups, Instagram, TikTok, LinkedIn, webinars, or influencer-style content. The law may define activities separately, but market execution often blends them together.

Financial Analysis — Advisory or Finfluencing?

Another major grey area is the interpretation of “Financial Analysis” or “Financial Consultation.” Some market participants associate this activity with traditional financial advisory services. Others attempt to position it closer to modern “finfluencer” culture — where individuals discuss markets, trading ideas, or investment opportunities through social media channels.

This distinction matters enormously from a regulatory perspective.

A regulated financial analyst , has to be approved by SCA, is generally expected to operate within a controlled compliance framework involving disclosures, research integrity, conflict management, documentation, and approved communication standards.

Who Owns These Category 5 Firms?

If one critically analyzes the ownership structures behind many Category 5 firms in the UAE market, an interesting trend emerges.

A large number of these entities are established by former sales heads, regional directors, relationship managers, business development executives, or senior market professionals previously associated with major brokerage brands such as Alpari, ADSS, MultiBank Group, and Equiti. A very few are actual Traders or Risk Experts.

These individuals possess extensive market experience, deep client networks, and strong understanding of sales-driven brokerage operations. BUT HONESTLY, NOT THE TRADERS AND THIS IS ONE OF TEH REASON THEY CANT STAY LONG WITHIN REGUALTORY FRAMEWORK. Naturally, many transitioned into establishing their own introducing or promotional businesses under the Category 5 framework.

From a business perspective, this evolution is understandable. However, from a compliance perspective, it introduces several concerns. One of the most debated issues is the overlap of Ultimate Beneficial Ownership (UBO) structures between introducing companies and the overseas brokerage entities to whom clients are introduced.

Technically, the introducing entity may state that it does not hold client assets or execute transactions. Yet commercially and strategically, the businesses may still remain interconnected through ownership, partnerships, commission arrangements, operational dependency, or group structures.

The concern becomes more pronounced where disclosures to clients are weak, transparency is limited, or conflicts of interest are not properly communicated.

The regulator’s focus today is not merely whether money flows through the introducer’s bank account. The broader concern is whether the client fully understands the nature of the relationship, the risks involved, and the commercial incentives behind the referral structure.

Application of Regulatory Laws — The Market Confusion

Another major challenge within the Category 5 ecosystem is regulatory interpretation. Many professionals entering the market are relatively new to compliance frameworks. The confusion often starts with a common misconception:

“We do not hold client money, so many AML obligations should not apply to us.”

Even some compliance officers struggle to practically interpret how UAE AML/CFT obligations apply to introducing businesses. In reality, UAE legislation frequently uses broad terminology such as “Licensed Financial Institutions” or “LFIs.” Once an entity falls under that regulatory classification, multiple obligations continue to apply irrespective of whether funds are directly handled.

This includes obligations related to (but not limited to):

- Customer due diligence (CDD)

- Sanctions screening

- Suspicious transaction reporting

- Risk assessment

- Compliance governance

- Staff training

- Record retention

- Transaction monitoring considerations

- Ongoing monitoring obligations

- Regulatory reporting expectations

The operational challenge becomes even heavier because many Category 5 firms operate cross-border introduction models. As a result, these entities often need to simultaneously comply with:

- UAE regulatory expectations; and

- The compliance standards of the foreign regulated brokerage or financial institution being promoted or introduced.

This creates duplication, operational burden, and sometimes conflicting interpretations of compliance obligations. For many smaller firms, the compliance cost itself becomes a major business challenge.

Warnings, Violations, and Regulatory Pressure

The market environment is changing rapidly.

Based on current industry observations, it appears that the Securities and Commodities Authority is now placing significantly greater scrutiny on Category 5 licensed firms. During past 3 years, 70% of the SCA licensed firms are Cat 5.

This is not surprising. A substantial portion of newly licensed entities in recent years fall within the Category 5 segment. At the same time, client complaints relating to aggressive marketing, misleading communication, offshore brokerage exposure, social media promotions, and high-risk trading losses have increased considerably. The regulator’s approach also appears faster and more proactive than before.

Inspections are becoming more frequent. Marketing practices are under greater review. Website structures, disclosures, onboarding methods, social media activities, and sales communication are receiving closer examination. The SCA license verification search now prominently displays warning notices and regulatory messaging before users proceed further into entity verification details.

This reflects a broader regulatory shift toward investor awareness, consumer protection, and reputational risk control. Many firms still underestimate this transition. Some continue operating with outdated assumptions that Category 5 is a “low-risk” or “light-touch” regulatory category. That perception is gradually disappearing.

Conclusion

The Category 5 licensing framework has undoubtedly opened opportunities for market growth, entrepreneurship, and financial sector expansion within the UAE. It has enabled experienced professionals to establish independent businesses and participate in regulated financial ecosystems without operating full brokerage infrastructures.

However, the same flexibility has also created significant grey areas. The boundaries between introduction, promotion, advisory, education, and digital influence are increasingly overlapping. Ownership structures, affiliate arrangements, offshore partnerships, and aggressive marketing models have further complicated the landscape.

At the same time, regulatory expectations are evolving rapidly.

The reality today is clear: Category 5 is no longer a “simple” license category. It is becoming one of the most scrutinized segments within the UAE financial services environment.

For firms operating in this space, survival will not depend only on sales performance or client acquisition. It will increasingly depend on governance, transparency, disclosure quality, compliance culture, and the ability to genuinely understand the spirit — not merely the wording — of UAE regulatory requirements.

The future of this sector will likely belong to firms that treat compliance not as a licensing formality, but as a core business function.

Post a comment

Related Posts

October 7, 2025

Strengthening Cybersecurity in UAE Insurance: What’s New??

1. Data Protection & Localization Under the updated Insurance Brokers’ Regulation (effective 15 February 2025), CBUAE now mandates…

June 4, 2025

Regulatory Update from DFSA

📢 Regulatory Update from #DFSA: Compliance Officer No Longer a Licensed Function The Dubai Financial…